Underpinning this improvement are reported higher cargo volumes and longer forward book orders signalling charterers recognition of the potential for vessel supply shortages ahead, especially for larger projects, and are locking in rates and cover earlier now than at any point so far in the recovery.

Looking back at 2021, MPP carriers can reflect on a feeding frenzy like nothing seen before. Even in the heady days of the late noughties – the last time MPPs really enjoyed any sustained momentum, the influencers were quite conventional: higher cargo demand was being met with more ships rolling out of yards.

2021’s meteoric rise has come from largely unconventional influencers, namely the impact of Covid. This has influenced the industry in many directions not least on the supply side where MPPs have been reappropriated to container feeders and older tonnage has been sold off to regional carriers at prices never thought possible. And with oil now close to $90 per barrel, this will surely stimulate investment in a sector that has provided consistent cargos and revenues to MPP/HL carriers for much of this millennium, but which have been absent for more than 5 years. What will be the effect when the oil & gas community compete with the renewable community for ship space?

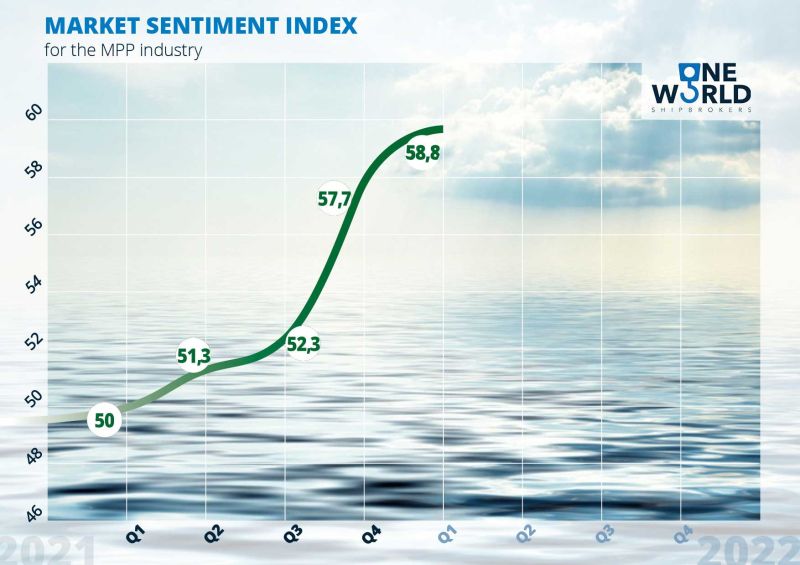

The forecast for the next MSI in April 2022 is for a small rise to 59.4.

The Market Sentiment Index is an indicator index of activity in the MPP industry. It averages the responses from an anonymous group of multipurpose vessel owner and operators to a set of breakbulk shipping-related questions. A reading of 50 is neutral, indicating a static market; scores below 50 show pessimism or wariness, and a score above 50 indicates optimism.

Read the full article here: https://breakbulk.news/charterers-lock-in-rates/

By Breakbulk